Business-to-business payments are financial transactions between two companies. Examples include a retailer paying a distributor, a manufacturer settling with a supplier, or a wholesaler purchasing inventory from a vendor.

Unlike consumer purchases that happen instantly at checkout, these transactions involve invoices, purchase orders, and negotiated terms. Buyers often pay weeks or months after receiving goods.

This guide covers how business-to-business payment processing works and the most common payment methods. It also covers key differences from B2C transactions and the trends shaping wholesale payments in 2026.

What Are B2B Payments

Business-to-business payments are financial transactions between two companies for goods or services—a market projected to reach $109.39 trillion in 2026. A manufacturer paying a supplier, a retailer settling an invoice with a distributor, a wholesaler purchasing inventory from a vendor. All of that falls under these transactions.

What separates B2B payments from the consumer transactions you’re used to? The short answer: complexity. When you buy something online as a consumer, you tap your card and you’re done.

In B2B, the transaction often involves purchase orders, invoices, and negotiated payment terms like Net 30 or Net 60. The buyer pays weeks after receiving the goods.

Here’s what makes these transactions distinct:

- Higher transaction values: Orders often run into thousands or hundreds of thousands of dollars

- Extended payment terms: Buyers typically pay 30, 60, or 90 days after delivery rather than at checkout

- Multi-step approval workflows: Finance teams review invoices and authorize payments before funds move

- Recurring relationships: The same buyer and seller transact repeatedly over months or years

Standard retail checkout wasn’t built for any of this. Wholesale buyers expect flexibility, and sellers who can’t offer it lose deals to competitors who can.

How B2B Payments Work

Wholesale payment processing moves through several stages, from the initial order all the way to reconciliation. Understanding each step helps you identify where friction slows things down—and where automation can speed things up.

Step 1. Purchase order and invoice issuance

The process starts when a buyer submits a purchase order specifying what they want, in what quantities, and at what agreed price. The seller then issues an invoice that includes the total amount due, payment terms, and payment deadline.

Step 2. Payment approval and authorization

Here’s where B2B diverges sharply from consumer transactions. The buyer’s finance team reviews the invoice, matches it against the original purchase order, and authorizes payment based on internal policies. For larger organizations, multiple approvers may be involved before anything moves forward.

Step 3. Payment execution and settlement

Once approved, funds transfer via the chosen method—ACH, wire, check, or card. Settlement timelines vary by method: ACH typically takes one to three business days, while wire transfers can settle same-day.

Step 4. Reconciliation and recording in ERP

Both parties match payments to invoices and record transactions in their ERP or accounting systems. When reconciliation is manual, errors creep in. When it’s automated, books stay accurate without the back-and-forth.

B2B Payments vs B2C Payments

Why can’t you just use your existing retail checkout for wholesale customers? The differences between B2B and B2C run deeper than transaction size.

For a comparison of B2B vs B2C payment differences, the U.S. Chamber of Commerce offers useful context.

| Factor | B2B Payments | B2C Payments |

|---|---|---|

| Transaction size | Larger order values | Smaller individual purchases |

| Payment timing | Net terms (pay later) | Pay at checkout |

| Approval process | Multi-step, cross-department | Single buyer decision |

| Payment methods | ACH, wire, net terms, RFQ | Credit card, debit, digital wallets |

| Buyer relationship | Ongoing, contract-based | Often one-time or sporadic |

| Invoicing | Required for every transaction | Rarely used |

The takeaway here is straightforward: wholesale transactions demand flexibility in terms, approval workflows, and integration with back-office systems. Standard B2C checkout doesn’t provide any of that.

Types of B2B Payment Methods

Businesses choose payment methods based on cost, speed, security, and buyer expectations. Here’s what you’ll encounter most often in wholesale and distribution. For a broader overview of B2B payment methods and trends, see Ramp’s guide.

ACH transfers

ACH (Automated Clearing House) moves money electronically between bank accounts through a batch processing network. It’s the workhorse of recurring supplier payments—lower fees than cards or wires, though settlement takes one to three days.

Wire transfers

When speed matters more than cost, wire transfers deliver. Funds settle same-day, making wires useful for large or international transactions. The tradeoff is higher fees, typically $15 to $50 per transfer.

Paper checks

Yes, checks still exist in B2B. They’re declining, however, because of fraud risk, manual processing, and slow clearing times. Many businesses are actively moving away from paper checks toward electronic alternatives.

Credit cards and virtual cards

Virtual cards generate one-time-use card numbers for each transaction, adding security and sometimes earning rebates. Traditional credit cards offer convenience but come with higher transaction fees—often 2% to 3% of the transaction value.

Net payment terms

Net 15, Net 30, Net 60—deferred payment arrangements let buyers pay by invoice after receiving goods. For wholesale and distribution, net terms aren’t a nice-to-have; they’re expected. A buyer who can’t pay on terms will often look elsewhere.

Real-time payments and digital wallets

Emerging options like RTP (Real-Time Payments) networks and B2B-focused digital wallets offer instant settlement. Adoption is growing. The FedNow Service now has over 1,400 participating institutions—particularly among businesses that want to eliminate waiting for funds to clear.

Quick comparison by priority:

- Lowest cost: ACH transfers

- Fastest settlement: Wire transfers or real-time payments

- Most flexibility: Net payment terms

- Highest security: Virtual cards

Common Challenges in B2B Payment Processing

If business-to-business payments were simple, you wouldn’t be reading this. Here’s what trips up most businesses:

- Manual processes: Paper-based invoicing and check handling slow operations and introduce errors at every step

- Fraud and security risks: Checks remain a primary target for B2B payment fraud, with losses running into billions annually

- Cross-border complexity: International payments involve multiple currencies, banking regulations, and longer settlement windows

- High transaction fees: Some methods carry steep costs that erode margins on lower-value orders

- Disconnected systems: Payments that don’t sync with ERP or CRM create reconciliation headaches and duplicate data entry

- Rigid checkout experiences: Lack of net terms or RFQ options causes wholesale buyers to abandon carts and call competitors instead

All of this is driving businesses toward automation, digital payment platforms, and integrated B2B ecommerce solutions that handle this complexity natively.

B2B Payment Trends to Watch

The wholesale payments landscape is shifting as businesses seek speed, security, and lower costs. Here’s what’s shaping the market heading into 2026. For a deeper look at how B2B payment processing works, Resolve Pay offers a detailed breakdown.

Shift to digital and real-time payments

Paper checks are fading—B2B check usage is down from 81% to 26% over the past two decades. Businesses are moving toward ACH, virtual cards, and real-time payment networks for faster, more secure transactions. The shift accelerated during the pandemic and hasn’t slowed down.

Embedded finance in B2B ecommerce

Embedded finance means integrating payment options—like net terms or buy-now-pay-later—directly into ecommerce checkout flows. Instead of handling terms offline through email or phone, buyers can select Net 30 at checkout and complete the order immediately.

Automation of AP and AR workflows

Electronic invoicing and automated approval workflows reduce manual effort, minimize errors, and accelerate cash flow. Businesses still running manual accounts payable processes are finding themselves at a disadvantage.

Rising B2B payment fraud and security demands

Fraud concerns are pushing businesses to adopt secure digital methods—79% of organizations experienced payment fraud in 2024 according to the AFP. Check fraud in particular is driving the shift to virtual cards and verified electronic payments with audit trails.

Growth of net terms and RFQ in online checkout

Wholesale buyers now expect to request quotes and pay on terms directly through ecommerce portals. If your checkout only accepts credit cards, you’re likely losing deals to competitors who offer more flexibility.

Modernizing your payment processes improves cash flow visibility, reduces administrative costs, and removes the uncertainty of manual, unverified processes.

How to Choose a B2B Payment Solution

Evaluating B2B payment tools? Here’s a practical framework for making the decision. You can also compare top B2B payment platforms to see how solutions differ.

1. Map your buyer segments and payment rules

Which customer groups expect net terms? Which pay by card? Which require RFQ for large orders?

Your solution has to support segment-specific pricing and payment rules—not one-size-fits-all checkout.

2. Verify ERP and CRM integration

Payments, invoices, and customer data have to sync with existing systems like NetSuite, Zoho, or Odoo. Without integration, you’re stuck with reconciliation chaos and manual data entry.

3. Evaluate security and fraud controls

Look for features like virtual card issuance, audit trails, and bank data verification. Security isn’t optional when transaction values run high.

4. Check net terms and RFQ support

Confirm that the solution can offer Net 15, Net 30, and Net 60 natively. Quote-to-order workflows should also be built in—not handled through workarounds outside the platform.

5. Assess total cost and settlement speed

Compare transaction fees, settlement timelines, and hidden costs across options. The cheapest method isn’t always the best fit for your buyer relationships.

Outcome: A solution that matches buyer expectations, integrates with your tech stack, and scales with wholesale operations.

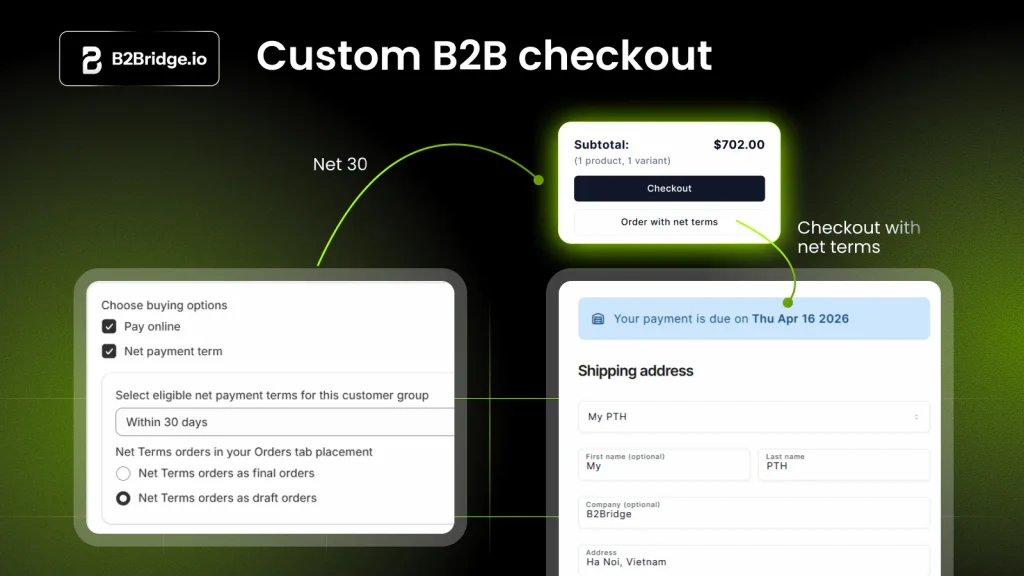

Running B2B Payments on Shopify with B2Bridge

If you’re running wholesale on Shopify, you’ve probably noticed that native checkout wasn’t built for B2B payment complexity. B2Bridge embeds flexible B2B paymentt options directly into Shopify—no separate platform, no Shopify Plus upgrade required.

Here’s what B2Bridge puts in your corner:

- Net payment terms: Offer Net 15, Net 30, and Net 60 to approved wholesale customers at checkout

- Request for Quote (RFQ): Let buyers submit quote requests that convert to draft orders

- Customer group payment rules: Assign different payment methods and terms by segment—VIP Distributors get Net 60 while Standard Wholesale pays by card

- ERP and CRM integration: Sync payments, invoices, and customer data with NetSuite, Zoho, Odoo, or custom systems

- Shopify-native checkout: Everything runs inside your existing store

Wholesale buyers get the payment flexibility they expect, and your team stops juggling spreadsheets and email threads.

Book A Demo to see how B2Bridge streamlines B2B payments for your wholesale operations.

Frequently Asked Questions about B2B Payments

How do net terms work in a B2B online checkout?

Net terms allow approved wholesale buyers to complete checkout without paying immediately. Instead, they receive an invoice with a due date—say, 30 days—and pay later via ACH, check, or wire transfer.

Is request for quote considered a B2B payment method?

RFQ isn’t a payment method itself. It’s a pricing negotiation workflow where buyers request custom pricing before the order is finalized and payment terms are applied.

How can merchants offer Net 30 only to approved wholesale customers?

Merchants use customer groups or tags to segment buyers. Net terms are assigned to specific groups, while other customers pay at checkout via card or ACH.

What is the difference between B2B payment processing and AP automation?

Business-to-business payment processing refers to the methods and systems that execute transactions between companies. AP (accounts payable) automation focuses on streamlining invoice approval, scheduling, and reconciliation workflows on the buyer side.

Hi, I’m Ha My Phan – an ever-curious digital marketer crafting growth strategies for Shopify apps since 2018. I blend language, logic, and user insight to make things convert. Strategy is my second nature. Learning is my habit. And building things that actually work for people? That’s my favorite kind of win.