Dual pricing is a strategy where businesses display two different prices for the same item: a lower price for cash payments and a higher price for credit card transactions. It’s legal in all 50 U.S. states and works as a cash discount program rather than a penalty for card use.

With processing fees climbing and margins tightening, more merchants are adopting dual pricing to recover costs without raising prices across the board. This guide covers how dual pricing works, how it compares to surcharging and cash discounting, and how to implement it in both retail and B2B operations.

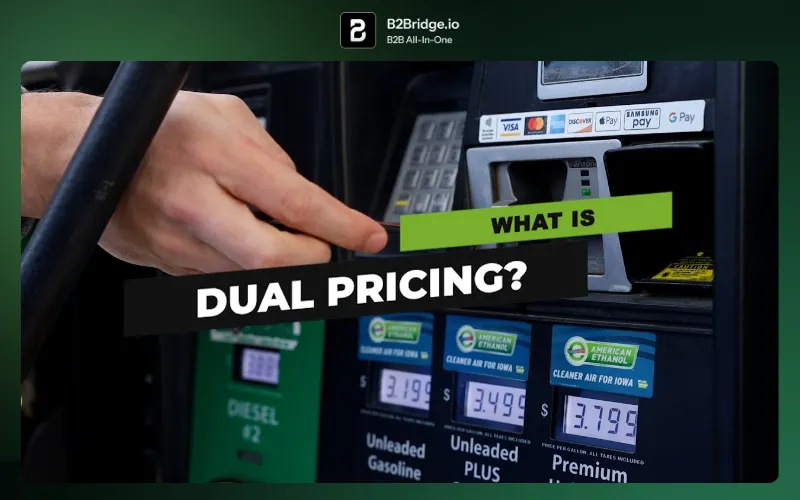

What Is Dual Pricing

Dual pricing is a strategy where businesses display two different prices for the same item: a lower price for cash payments and a higher price for credit card transactions. The practice is legal in all 50 U.S. states and works as a cash discount program rather than a penalty for card use.

The idea is simple. You set your card price as the standard rate—the one that accounts for processing fees—and then offer a reduced cash price to customers who skip the card. This lets you recover transaction costs without raising prices across the board for everyone.

Think of it like gas station pricing, where you’ve probably seen one price for cash and another for credit. That same model now shows up in restaurants, retail stores, and increasingly in ecommerce.

- Cash price: The lower amount customers pay when using cash or debit

- Card price: The higher amount that covers credit card processing costs

- Display requirement: Both prices shown upfront before the customer commits

How Dual Pricing Works

You start with your card price as the base. This is the price that includes your processing fee margin, typically around 3–4%. From there, you calculate the cash price by subtracting that fee offset.

When a customer pays with cash, they get the lower price. When they pay by card, they pay the posted card price. No surprise fees at checkout, no hidden charges—just two clearly displayed options and a choice.

The flow looks like this: your POS system or signage shows both prices, the customer picks their payment method, and the system applies the correct amount automatically.

What Is Dual Pricing Credit Card Processing

This term refers to how payment processors and POS systems handle dual pricing on the technical side. The system calculates and displays both prices, then applies the right amount at checkout based on how the customer pays.

If you’re working with a merchant services provider, dual pricing credit card processing is how they’ll describe the setup. Your processor configures your terminal or ecommerce checkout to show both price points and route the transaction accordingly.

Dual Pricing vs Surcharging vs Cash Discounting

These three terms get mixed up constantly, and the distinctions matter for compliance.

| Method | How It Works | Legal Status |

|---|---|---|

| Dual Pricing | Two prices displayed upfront (cash and card) | Legal in all 50 U.S. states |

| Surcharging | Fee added at checkout only for card payments | Restricted or banned in some states |

| Cash Discounting | Card price is base; discount applied for cash | Legal in all 50 U.S. states |

Dual Pricing vs Surcharging

Surcharging adds a fee at the end of the transaction specifically for card users. Some states ban surcharging entirely, and card networks have strict rules around it.

Dual pricing sidesteps those issues by showing both prices upfront. You’re not penalizing card users—you’re displaying two price options and letting customers choose before they reach the register.

Dual Pricing vs Cash Discounting

Cash discounting and dual pricing are closely related. The difference is subtle: cash discounting specifically frames the card price as the base and offers a discount for cash, while dual pricing displays both prices without necessarily using discount language.

In practice, the outcome is the same. The framing just shifts depending on how you communicate it.

Dual Pricing vs Tiered Pricing

Tiered pricing refers to volume-based or customer-group-based price levels, which is common in B2B and wholesale. A retailer might pay one price, a distributor another, and a VIP account a third.

This differs from payment-method pricing, though the two can work together. A wholesale buyer might see tiered pricing based on their customer group and dual pricing based on how they pay.

Is Dual Pricing Legal

Yes. Dual pricing is legal in all 50 U.S. states because it’s framed as a discount for cash rather than a penalty for cards. This distinction separates it from surcharging, which faces state-level restrictions.

Compliance still requires attention to detail:

- Signage: Both prices displayed clearly before checkout

- Receipt clarity: Final price matches the displayed price for the chosen payment method

- Card network rules: Visa, Mastercard, and other networks have guidelines around disclosure

The key is transparency. As long as customers see both prices upfront and understand what they’re paying, you’re operating within the rules.

Key Benefits of Dual Pricing for Merchants

Protected Margins on Every Transaction

Credit card processing fees typically run 2–4% per transaction. Dual pricing lets you recover those costs from card-paying customers without raising your base prices for everyone else.

Transparent Pricing for Customers

Customers see both prices before they buy. This transparency tends to reduce complaints compared to surcharging models where fees appear at the last moment.

Higher Cash Conversion

Cash-paying customers benefit from lower prices, and the incentive often shifts payment behavior toward cash. This reduces your overall processing costs.

Predictable Profitability Across Payment Methods

Your profit margins stay consistent regardless of how customers pay. A $100 sale nets you roughly the same profit whether the customer uses cash or card.

Flexibility Across Customer Segments

Dual pricing works for both retail and wholesale customers. You can layer it with customer-group pricing strategies to create segment-specific approaches.

Why More Merchants Are Adopting Dual Pricing

Processing fees reached a record $148.5 billion in 2024, and they squeeze margins—especially for businesses with tight profit windows. Dual pricing offers a compliant way to offset those costs.

You’ve probably noticed dual pricing at gas stations for years. With consumers averaging 17 credit card payments per month, it’s now spreading to restaurants, retail stores, and ecommerce. Modern POS systems and payment processors have made implementation far easier than it used to be.

The math is compelling. A business processing $500,000 annually in card transactions at 3% fees pays $15,000 a year in processing costs. Dual pricing can recover most or all of that.

How to Implement Dual Pricing in Your Business

Step 1: Audit Your Current Pricing and Processing Costs

Review your existing product prices and calculate your average credit card processing fees. Understanding the margin gap is the foundation for setting your dual pricing structure.

Step 2: Choose Your Dual Pricing Model

Decide whether to show cash and card prices side-by-side or use a percentage-based discount for cash. Both approaches work—the choice often comes down to how your POS system handles the display.

Step 3: Configure Price Lists and Customer Groups

Set up your system to support two price tiers. For B2B merchants on Shopify, this might mean creating customer groups or price lists for different buyer types, which can then layer with payment-method pricing.

Step 4: Update Storefront and Checkout Displays

Both prices need to be visible on product pages, at POS terminals, and during checkout. Signage has to be clear—ambiguity creates compliance risk and customer frustration.

Step 5: Communicate the Change to Customers

Notify existing customers about the new pricing structure before it takes effect. Frame it as a cash discount rather than a card penalty.

Step 6: Monitor Performance and Adjust

Track your payment method mix, customer feedback, and margin impact after launch. Adjust pricing or messaging based on what the data shows.

Common Mistakes to Avoid With Dual Pricing

Failing to Disclose the Price Difference

Both prices have to be displayed clearly. Hidden fees create compliance problems and customer complaints—exactly what dual pricing is designed to avoid.

Mixing Up Surcharging and Dual Pricing Rules

Surcharging has different legal requirements and state restrictions. Applying surcharge logic to a dual pricing setup can create compliance trouble.

Overlooking State and Card Network Compliance

Even though dual pricing is broadly legal, card networks have specific guidelines around signage and disclosure. Verify the rules before you launch.

Showing B2B Prices to Retail Shoppers

If you’re offering wholesale dual pricing, those prices typically need to stay hidden from B2C customers. Exposing wholesale rates to retail shoppers creates channel conflict and erodes margins.

Dual Pricing for B2B and Wholesale on Shopify

In B2B contexts, dual pricing often means something broader: showing different prices to different customer groups, such as wholesale vs. retail, rather than only cash vs. card.

Customer Group and Role Based Price Lists

You can assign specific price lists to customer groups, so wholesale buyers see lower prices than retail shoppers. This is standard practice for distributors and manufacturers selling to multiple buyer types.

Hidden Wholesale Prices for B2C Shoppers

B2B pricing typically stays invisible to public or retail visitors. Only verified wholesale accounts see those prices, which protects margins and prevents channel conflict.

Multi Currency and Tax Exempt Pricing

International wholesale buyers often need localized pricing and tax-exempt logic. Supporting multiple currencies and tax configurations is essential for global B2B operations.

ERP and CRM Aligned Pricing

Price lists and customer groups work best when they sync with your ERP or CRM. Keeping pricing consistent across platforms reduces errors and saves operational time.

Run Dual Pricing on Shopify With B2Bridge

B2Bridge brings enterprise-grade pricing capabilities to Shopify merchants running B2B operations. You can set up customer-group pricing, hide wholesale prices from retail shoppers, and sync price lists with your ERP—all without requiring Shopify Plus.

- Customer-group pricing: Assign different price lists to wholesale, retail, and VIP accounts

- Hidden pricing: Keep B2B prices invisible to unapproved visitors

- ERP integration: Sync with NetSuite, Zoho, Odoo, or custom systems

- Multi-currency support: Price in local currencies for international buyers

- Net payment terms: Offer Net 30/60/90 alongside your pricing structure

Contact us to get expert guidance on setting up dual pricing for your wholesale store.

Frequently Asked Questions About Dual Pricing

How is dual pricing displayed on a product page?

Both the cash price and card price appear on the product page or at the point of sale, so customers see the difference before selecting a payment method. The display format varies by POS system.

Can I run dual pricing without Shopify Plus?

Yes. Apps like B2Bridge let standard Shopify merchants set up customer group pricing and tiered price lists without requiring Shopify Plus or a separate B2B storefront.

Does dual pricing work for online and ecommerce stores?

Dual pricing can be implemented in ecommerce by displaying both prices on product pages and applying the correct price at checkout based on payment method or customer group.

Can dual pricing apply to international or multi-currency customers?

Yes. Merchants can configure dual pricing alongside multi-currency settings to show localized prices for international wholesale or retail buyers.

Does dual pricing affect customer loyalty?

When presented transparently, dual pricing typically doesn’t harm loyalty. Many customers appreciate the option to save by paying with cash or qualifying for wholesale rates.

Hi, I’m Ha My Phan – an ever-curious digital marketer crafting growth strategies for Shopify apps since 2018. I blend language, logic, and user insight to make things convert. Strategy is my second nature. Learning is my habit. And building things that actually work for people? That’s my favorite kind of win.