Credit card payments are usually processed within 1-3 business days, though authorization happens almost instantly. The total time may vary depending on the payment method, transaction timing, and delays caused by weekends, holidays, or fraud verification. Misunderstanding these timelines can lead to unnecessary late fees, interest charges, and even negative impacts on your credit score.

In this comprehensive guide, we’ll break down exactly how long do credit card payments take, what happens when you process credit card payments, typical timeframes you can expect, and practical strategies to ensure your payments are processed quickly and safely.

What Does It Mean to Process Credit Card Payments?

Before answering how long does it take to process credit card payment, it’s essential to understand what happens behind the scenes when you make a payment.

Defining Payment Crediting vs Processing

Many people confuse payment crediting with payment processing, but these are two distinct stages that affect how long credit card payments take overall.

Credited payment occurs when your credit card balance is updated to reflect your payment. This is what you see in your account – your available credit increases, and your outstanding balance decreases. Crediting can happen relatively quickly, sometimes within hours of making a payment.

Processed payment, on the other hand, refers to the complete journey of funds from your bank account to the credit card issuer, including verification, clearing, and settlement. This is when the money actually moves between financial institutions and is fully reconciled.

Key differences:

- Crediting provides immediate balance relief but doesn’t mean funds have transferred

- Processing involves actual fund movement and can take 1-5 business days

- Crediting allows you to use the freed-up credit line sooner

- Processing determines when your bank account is actually debited

- Failed processing can reverse a credit if funds are insufficient or invalid

>> Read more: B2B Ecommerce in 2026: What It Is and How to Start

Overview of Credit Card Payment Processing Flow

When you process payments on your credit card, the transaction goes through several stages:

1. Authorization – You initiate the payment through your bank’s website, app, or payment portal. The system verifies your account details and confirms sufficient funds are available.

2. Batching – Your payment is grouped with other transactions in a batch. Banks typically process payments in batches at specific times throughout the day rather than individually.

3. Clearing – The payment information is sent through the payment network (like ACH for bank transfers or card networks for card payments) to be matched and verified between institutions.

4. Settlement – Funds are actually transferred from your bank account to the credit card issuer. This is when the transaction is finalized and reconciled in both institutions’ systems.

5. Posting – The payment officially posts to your credit card account, and all records are updated permanently.

Transform your B2B store with B2Bridge.

Discover how B2Bridge can transform your wholesale business.

Schedule a demo today to see our payment management tools in action.

How Long Do Credit Card Payments Take? Typical Timeframes For Processing Payments

The answer to how long credit card payments take depends significantly on whether you’re making same-bank or interbank payments.

Same-Bank Payments

When your checking account and credit card are with the same financial institution, payment processing is significantly faster. These payments can be credited almost instantly or within the same business day.

For example, if you have both a Chase checking account and a Chase credit card, your payment might be credited within minutes to a few hours. The bank doesn’t need to coordinate with external institutions, allowing them to update both accounts within their own system quickly. Many major banks like Bank of America, Wells Fargo, and Citibank offer same-day crediting for same-bank payments made before their cut-off times.

This speed advantage makes same-bank arrangements particularly attractive for people who want maximum control over their payment timing and available credit.

Interbank Payments

For most people wondering how long credit card payments take, interbank payments are the relevant scenario. These payments typically take 1 to 3 business days to fully process when your bank and credit card issuer are different institutions. This is the most common scenario for many consumers who may bank with one institution but have credit cards from various issuers.

The extended timeline exists because the payment must travel through intermediary payment networks, be verified by multiple parties, and clear through systems like the Automated Clearing House (ACH). On day one, you initiate the payment and it may be credited to your card balance. On day two, the clearing process occurs. By day three, the funds are typically settled and transferred between banks.

Some factors that can extend this timeline include:

- First-time payments to a new payee may require additional verification

- Large payment amounts might trigger security reviews

- International banks or less common financial institutions may have slower processing agreements

Impact of Cut-off Times, Weekends, and Holidays

Understanding how timing affects payment processing is critical for avoiding late payments and managing your available credit effectively.

| Timing Factor | Impact on Processing |

| Before cut-off time | Payment credited same business day or next business day |

| After cut-off time | Payment processed as if made the next business day |

| Weekends | Payments made Saturday/Sunday process on Monday |

| Bank holidays | Add an extra business day to processing time |

| End of month | Higher transaction volumes may cause slight delays |

Most banks have cut-off times between 5:00 PM and 8:00 PM Eastern Time for same-day crediting. Payments made after these times are typically batched with the next business day’s transactions. During holiday periods like Thanksgiving or Christmas, plan for an additional 1-2 business days beyond the normal processing time.

Why Do Credit Card Payments Take So Long to Process?

You might wonder why, in an age of instant digital communication, it takes days to process payments. Several important reasons explain these timelines.

The financial system prioritizes security and accuracy over speed. Each payment must be verified, authenticated, and reconciled to prevent fraud, errors, and financial crime. Banks and payment processors implement multiple checkpoints to ensure the right amount leaves the right account and arrives at the correct destination.

Key reasons for processing delays:

- Fraud prevention measures – Systems scan for suspicious activity and unusual patterns that might indicate fraud or unauthorized access

- Regulatory compliance – Financial institutions must comply with anti-money laundering (AML) and Know Your Customer (KYC) regulations

- Batch processing systems – Many banks still use legacy systems that process transactions in scheduled batches rather than real-time

- Inter-bank coordination – Multiple institutions and payment networks must communicate and reconcile transactions

- Settlement risk management – Banks ensure funds are actually available before finalizing transfers

- Network operating hours – Payment networks like ACH have specific operating windows and don’t process 24/7

- Volume management – Banks process millions of transactions daily and must organize them systematically

While these timeframes may seem inconvenient, they represent a careful balance between speed, security, and operational reliability in the financial system.

If you’re managing wholesale operations and struggling with complex payment terms, slow processing, and manual reconciliation, B2Bridge can help. Our all-in-one wholesale management app automates payment processing and manages customer credit terms.

Common Factors Influencing Credit Card Payment Processing Speed

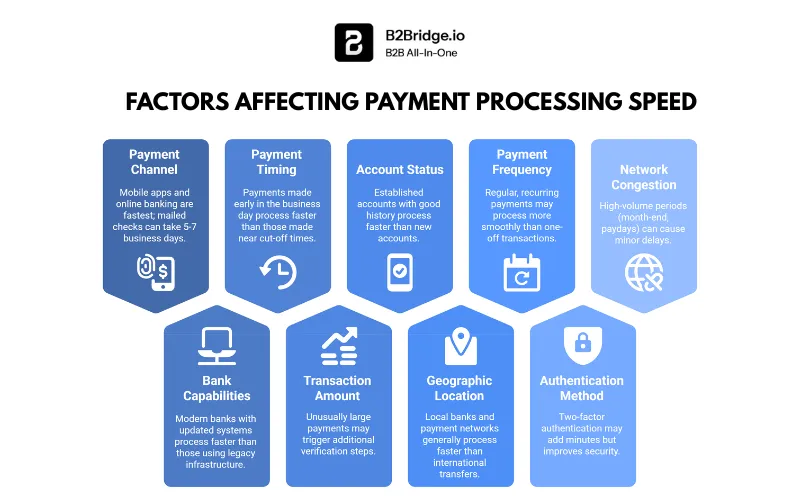

Beyond the standard timelines, several specific factors can accelerate or delay how quickly your credit card payments process.

Your chosen payment method significantly impacts processing speed. Digital payment channels like bank apps, online banking portals, and real-time payment systems generally process faster than traditional methods like mailing checks or making payments through third-party services.

Major factors affecting processing speed:

- Payment channel used – Mobile apps and online banking are fastest; mailed checks can take 5-7 business days

- Bank’s processing capabilities – Modern banks with updated systems process faster than those using legacy infrastructure

- Payment timing – Payments made early in the business day process faster than those made near cut-off times

- Transaction amount – Unusually large payments may trigger additional verification steps

- Account status – Established accounts with good history process faster than new accounts

- Geographic location – Local banks and payment networks generally process faster than international transfers

- Payment frequency – Regular, recurring payments may process more smoothly than one-off transactions

- Authentication method – Two-factor authentication may add minutes but improves security

- Network congestion – High-volume periods (month-end, paydays) can cause minor delays

Regional payment systems also play a role. In Singapore and some other Asian markets, systems like FAST (Fast and Secure Transfers) and PayNow enable near-instant processing for participating banks. In the US, the Real-Time Payments (RTP) network and Same Day ACH services are gradually reducing processing times.

Tips to Ensure Your Credit Card Payments Process Quickly and Safely

Taking proactive steps can help you minimize processing delays and ensure your payments post on time, every time.

Use Faster Payment Channels

Modern payment technologies offer significantly faster processing than traditional methods. Leveraging these channels can give you more control over your payment timing.

Recommended fast payment options:

- Bank mobile apps – Most major banks credit payments made through their apps within hours during business days

- Online banking portals – Direct bank-to-bank transfers through secure web platforms offer fast, trackable payments

- Real-time payment systems – Services like Zelle, PayNow, or FAST provide immediate or same-day processing

- Electronic funds transfer (EFT) – Automated transfers that process faster than checks or manual methods

- Bill pay services – Bank-integrated bill pay can schedule and process payments efficiently

- Card network payment options – Some issuers offer debit card payment options that process within 24 hours

Avoid mailing physical checks whenever possible, as these can take 5-7 business days to process and carry risks of loss or theft in transit.

Pay Before Cut-off Times

Every bank has specific cut-off times after which payments are processed the next business day. Knowing and respecting these times is crucial for time-sensitive payments.

Common cut-off times by bank type:

| Bank Type | Typical Cut-off Time | Crediting Timeline |

| Major national banks | 5:00 PM – 8:00 PM ET | Same day or next day |

| Regional banks | 3:00 PM – 6:00 PM local time | Same day or next day |

| Credit unions | 2:00 PM – 5:00 PM local time | 1-2 business days |

| Online-only banks | 8:00 PM – 11:59 PM ET | Next business day |

Check your specific bank’s cut-off times in their online banking portal or mobile app. Many banks display this information prominently on their payment pages. When making time-critical payments, aim to submit them by early afternoon to ensure they’re included in the same day’s batch processing.

Use Automatic Payments and Set Reminders

Automation removes the human error factor from payment timing and ensures you never miss a due date due to forgetfulness or scheduling conflicts.

Benefits of automation:

- Guaranteed on-time payments – Automated payments process on schedule without requiring your intervention

- Improved credit score – Consistent, timely payments positively impact your payment history

- Reduced late fees – Eliminate the risk of forgetting a payment deadline

- Better cash flow management – Predictable payment schedules help you plan expenses

- Peace of mind – One less financial task to track manually

- Qualification for benefits – Some card issuers offer interest rate reductions for automatic payment enrollment

Best practices for automated payments:

- Set up autopay for at least the minimum payment to protect your credit score

- Schedule payments 3-5 days before the due date to account for processing time

- Maintain sufficient buffer funds in your payment account

- Review statements monthly even with autopay to catch fraudulent charges

- Set calendar reminders to verify payments processed successfully

- Keep backup payment methods available in case primary method fails

What To Do If Your Payment Is Delayed

Despite careful planning, payment delays can occasionally occur. Knowing how to respond quickly can minimize negative consequences.

Initial Check and Verification Steps

Before contacting your bank, perform these verification steps to understand where your payment stands:

- Check your transaction history in your bank account to confirm the payment was actually submitted and authorized

- Review your credit card account to see if the payment has been credited even if not fully processed

- Verify confirmation numbers from your payment submission – save these for reference

- Check for error messages in your banking app or email that might explain the delay

- Confirm sufficient funds were available in your account when the payment was initiated

- Review cut-off times to determine if your payment was made after the processing window

- Account for weekends and holidays that might extend normal processing timelines

- Check your email for any communication from your bank about verification needs or issues

Most apparent “delays” are actually normal processing times, especially for interbank payments made near cut-off times or on weekends.

When and How to Contact Your Bank

If your payment hasn’t been credited within the expected timeframe (3-5 business days for interbank transfers), it’s time to contact your financial institution.

Contact your bank when:

- More than 5 business days have passed with no credit

- Your payment shows an error status

- Funds were debited from your account but not credited to your card

- You receive notification of a failed payment

Information to provide:

- Confirmation or reference number from your payment submission

- Exact date and time you initiated the payment

- Payment amount and source account details

- Credit card account number and issuer information

- Screenshots of transaction history showing the payment status

Most banks can trace payments through their systems and provide specific information about where the payment is in the processing pipeline. They can also expedite processing or issue provisional credits if an error occurred on their end.

Avoiding Duplicate Payments

When payments appear delayed, a common mistake is submitting a second payment, which can create financial complications and overdraft issues.

Risks of duplicate payments:

- Overpayment creating a negative balance on your credit card

- Insufficient funds if your bank account can’t cover both payments

- Overdraft fees from your bank if the second payment exceeds available funds

- Complicated refund process to recover overpaid amounts

- Delayed fund availability while refunds are processed

Prevention strategies:

- Wait the full processing timeframe (5 business days) before attempting another payment

- Use confirmation numbers to verify payment submission rather than relying on memory

- Keep detailed records of all payment submissions with dates and amounts

- Enable payment notifications in your banking app

- Contact your bank for payment status before submitting duplicates

If you accidentally submit a duplicate payment, contact both your bank and credit card issuer immediately. Many can cancel the second payment if it hasn’t been processed, or expedite a refund if both payments have cleared.

Special Considerations for Wholesale B2B Payment Processing

While the question “how long do credit card payments take?” for consumers typically involves days, wholesale and B2B transactions operate on significantly different timelines and structures.

In wholesale B2B commerce, payment processing involves more than just crediting payments – it encompasses extended payment terms, credit lines, invoicing systems, and complex reconciliation processes. Wholesale buyers often receive net payment terms that allow them to receive goods or services immediately but pay weeks or months later. This creates unique cash flow challenges for suppliers who must manage inventory, production, and operational costs while waiting for payment.

The payment processing infrastructure for B2B also differs substantially. While consumer payments go through card networks and ACH systems, B2B payments might involve wire transfers, EDI (Electronic Data Interchange) systems, trade credit arrangements, and specialized B2B payment platforms. Processing times can range from same-day wire transfers to 90+ days for extended net terms.

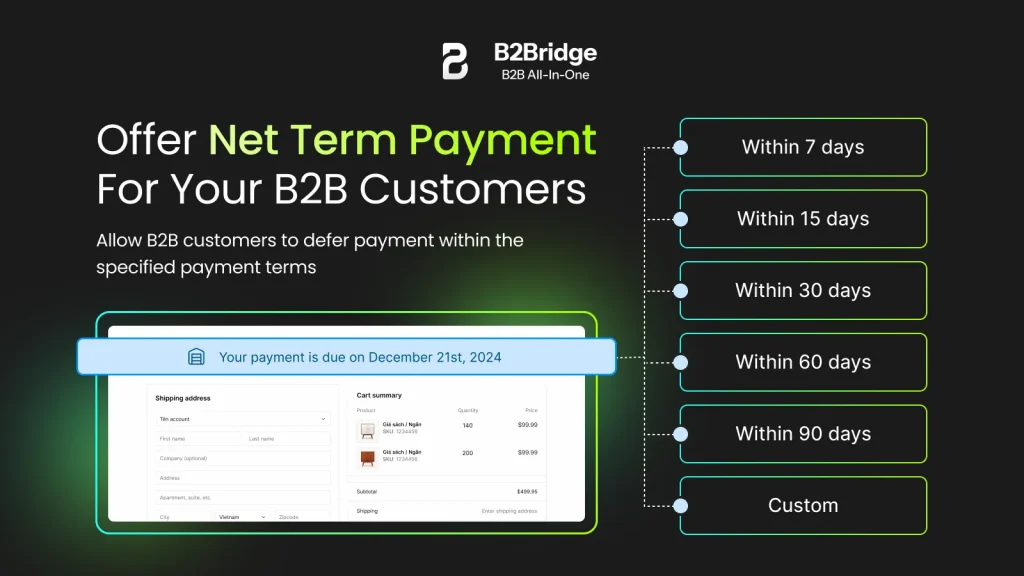

Net Payment Terms and Their Role (Net 30, Net 60, Net 90)

Net payment terms are standard in wholesale transactions and define when payment is due relative to the invoice date or delivery date.

Net 30 means payment is due 30 days after the invoice date. This is the most common term in B2B commerce, providing buyers with a month to inspect goods, process paperwork, and arrange payment while giving suppliers reasonable cash flow predictability.

Net 60 extends the payment window to 60 days, often used for larger orders, established customer relationships, or industries with longer sales cycles. This provides buyers with more working capital flexibility but requires suppliers to have stronger cash reserves.

Net 90 represents a three-month payment window typically reserved for very large orders, strategic partnerships, or situations where buyers have significant negotiating leverage. While this benefits buyer cash flow substantially, it can strain supplier finances and working capital.

These terms fundamentally change the concept of “processing time” in B2B contexts. Rather than waiting 1-3 days for payment to clear, suppliers may wait 30-90 days just for payment to be initiated, plus additional processing time once the payment is submitted.

Trends in Wholesale Pricing and Payment Flexibility

The wholesale B2B payment landscape is evolving rapidly, driven by technology, changing buyer expectations, and competitive pressures.

Emerging trends in wholesale payments:

- Dynamic discounting – Suppliers offer discounts (e.g., 2/10 Net 30) for early payment, improving their cash flow while reducing buyer costs

- Flexible payment terms – Customized payment schedules based on buyer creditworthiness and order history

- Digital payment platforms – Shift from checks and wire transfers to integrated digital payment systems

- Supply chain financing – Third-party financing options that pay suppliers immediately while extending terms for buyers

- Installment payment plans – Breaking large orders into manageable monthly payments

- Cryptocurrency and blockchain – Emerging options for international B2B transactions with faster settlement

- Automated reconciliation – AI-powered systems that match payments to invoices automatically

- Real-time payment tracking – Visibility into payment status throughout the processing lifecycle

These trends reflect a broader movement toward making B2B payment processing more efficient, transparent, and flexible – addressing the traditional pain points of extended payment terms and complex reconciliation processes.

How B2Bridge Helps Simplify and Automate Wholesale Payment Management

For wholesale businesses struggling with complex payment processing, extended terms, and manual reconciliation, B2Bridge Shopify App offers comprehensive solutions.

B2Bridge provides a complete ecosystem for managing wholesale operations, with particular strength in payment processing and financial management. For wholesale businesses processing credit card payments alongside traditional net terms, B2Bridge provides the infrastructure to manage both seamlessly.

Key features include flexible payment term configuration, integrated payment processing supporting multiple payment methods, customer credit limit management, and detailed financial reporting. By automating payment workflows, B2Bridge helps suppliers reduce processing time from days to hours, minimize payment errors and disputes, improve cash flow visibility, reduce manual accounting work, and offer customers more payment flexibility.

Whether you’re a supplier looking to offer competitive payment terms while maintaining healthy cash flow, or a wholesale buyer seeking better visibility into your payment obligations, integrated wholesale management Shopify apps like B2Bridge are transforming how the industry handles payment processing.

FAQs about Process Credit Card Payments

To process credit card payments, a business uses a payment gateway and processor to verify transaction details, authorize payment, and transfer funds from the customer’s card to the merchant’s account, ensuring security and compliance throughout the process.

Most credit card payments take one to three business days to process. However, processing time depends on the payment processor, bank policies, and transaction type – some providers may offer instant or same-day payouts for an additional fee.

Stripe typically processes payments within two business days for established businesses. New accounts or certain industries may experience longer initial payouts of up to seven days while Stripe verifies account information and assesses potential risk.

Credit card payments typically show on your account (credited to your balance) within a few hours to one business day, though full processing takes 1-3 business days. Same-bank payments credit fastest, often within hours. Interbank payments usually credit within 24 hours but take 1-3 business days to fully settle.

Your available credit typically updates within a few hours to one business day after your payment is credited, even though full processing may take longer. For same-bank payments, credit may be available almost immediately. For interbank payments, expect your credit limit to update within 24 hours of crediting

Your available credit typically updates within a few hours to one business day after your payment is credited, even though full processing may take longer. For same-bank payments, credit may be available almost immediately. For interbank payments, expect your credit limit to update within 24 hours of crediting, though the payment may still be processed in the background.

Late payments generally aren’t reported to credit bureaus until they’re 30 days past due. However, you may incur late fees as soon as you miss your due date. To protect your credit score, always make at least the minimum payment by the due date, accounting for processing times by paying 3-5 days in advance.

Bank mobile apps and online banking portals typically offer the fastest processing, especially for same-bank payments. Real-time payment systems like Zelle or FAST can provide same-day processing. Debit card payments to credit cards can be processed within 24 hours. Wire transfers are fastest for large amounts but may incur fees. Physical checks are slowest, taking 5-7 business days.

No, most credit card payments don’t process on weekends or bank holidays. Transactions made during those times are typically queued and processed on the next business day when banks and payment networks resume operations.

To process credit card payments over the phone, use a virtual terminal or POS system. Collect the customer’s card details, enter them manually, verify authorization, and confirm the transaction securely following PCI compliance standards.

Credit card payments can take time to process because transactions are handled in batches, banks operate only on business days, security checks may be required, and multiple financial institutions are involved. As a result, payments typically take 1–5 business days to fully settle.

Conclusion

Understanding how long it takes to process credit card payments – and the factors that influence these timelines – empowers you to manage your finances more effectively and avoid costly mistakes. The key to successful payment management is planning ahead. Make payments well before due dates, use fast payment channels when possible, set up automation to ensure consistency, and maintain detailed records of your transactions. For B2B wholesale operations, understanding extended payment terms and leveraging integrated payment management platforms can transform cash flow and operational efficiency.

Whether you’re a consumer managing personal credit cards or a business processing wholesale payments, the principles remain the same: understand the process, plan for processing times, and use technology to your advantage.

Hi, I’m Ha My Phan – an ever-curious digital marketer crafting growth strategies for Shopify apps since 2018. I blend language, logic, and user insight to make things convert. Strategy is my second nature. Learning is my habit. And building things that actually work for people? That’s my favorite kind of win.